Determination of Money Supply in Nepal

Introduction

Money Supply is defined as the total money in circulation within the economy during the given period. It is determined jointly by the behaviour of the general public, government, banks, and Financial Institutions (BFIs), and the policy of the central bank. The Central Bank’s policy is said to be dominant in determining the money supply, and so the money supply is said to be a policy choice variable.

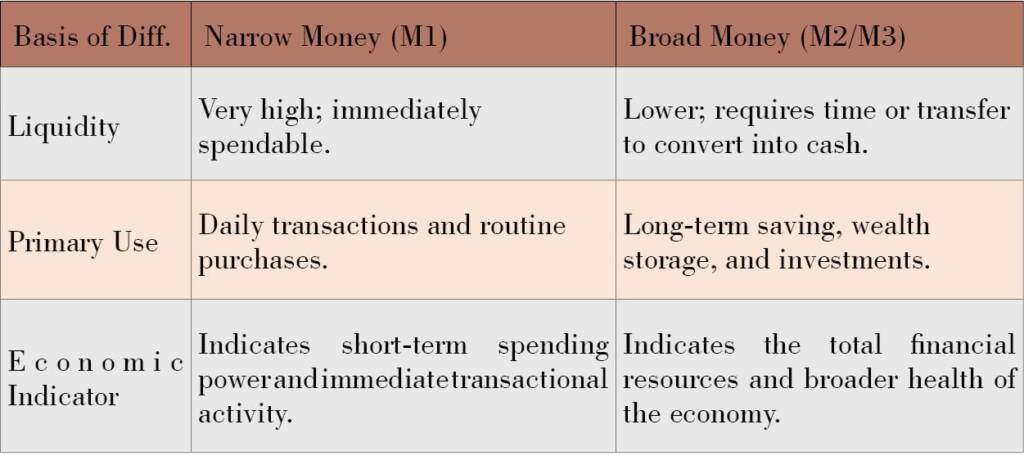

For the purpose of accounting and policy-making, money supply is classified into narrow and broad money, where narrow money is highly liquid and acceptable in every transaction, but broad money is less liquid, i.e.

| Narrow Money (M1) = C + DD |

| Broad Money(M2) = M1 + TD |

| M3 = M2 + FOREX |

where,

C = Cash held by the general public

DD = Demand deposits (cheque-based transactions and digital transactions)

TD = Time deposits (fixed deposits)

FOREX = Foreign exchange reserves

Key Differences between Narrow Money and Broad Money:

| Basis of Diff. | Narrow Money (M1) | Broad Money (M2/M3) |

| Liquidity | Very high; immediately spendable. | Lower; requires time or transfer to convert into cash. |

| Primary Use | Daily transactions and routine purchases. | Long-term saving, wealth storage, and investments. |

| Economic Indicator | Indicates short-term spending power and immediate transactional activity. | Indicates the total financial resources and broader health of the economy. |

High Power Money (H) Theory: H- Theory of Money Supply

High-power money is defined as money with the power of credit creation. It is the money held by the general public and the total reserves in the banking system.

| H= C+R |

where,

C = Cash held by the general public

R = Total reserve ( required + excess reserve in banks)

This means high-powered money is the total currency in circulation within the economy, which includes both physical and digital currency in the market. The H-Theory of money supply shows that there is a positive relationship between money supply and high-powered money, i.e.

MS = f (H), f’> 0

If H increases, then MS also increases.

If H decreases, then MS also decreases.

As there is a positive relationship between the money supply and high-powered money, the factors affecting H are also the factors affecting the money supply. There are both supply (source) and demand (use) side factors of H that affect the money supply. In order to explore such supply and demand side factors of H, we have to examine the Balance Sheet of the Central Bank.

Balance Sheet of the Central Bank:

| Assets = Liabilities |

Monetary Assets+Non-Monetary Assets = Monetary Liabilities + Non-Monetary Liabilities

| MA+ NMA = ML + NML |

The MA represents the source or supply side factors of H, and it consists of:

MA = NFA + NCG + CGE + CCB + CPS

where,

NFA = Net Foreign Assets

NCG = Net Credit to Government

CGE = Credit to Government Enterprises

CCB = Credit to Commercial Banks

CPS = Credit to the Private Sector

Here, NFA and NCG are exogenous, whereas CGE, CCB, and CPS are endogenous factors.

These supply-side factors of H have a positive effect on the money supply. If NFA increases due to increased inflow of remittances, tourism income, foreign investment, foreign aid, and exports, it increases the high-powered money and the money supply in the economy. Similarly, if the government borrows more money from the central bank (NCG increase), it increases the money supply. Similar is the case with other supply factors of H.

Similarly, ML of the central bank represents demand or uses of H, and it consists of:

| ML = CP + RG + RB + VCB + RP |

where,

CP = Cash held by the general public

RG = Reserve of the Government with the central bank

RB = Reserve of banks with the central bank

VCB = Vault cash of banks

RP = Reserve of private sector with the central bank

Here, CP and RG are the exogenous variables, whereas RB, VCB, and RP are the endogenous variables.

There is an inverse relationship between the money supply and these demand-side factors of H. It means that if the public starts holding more cash ( CP increases), it reduces the circulation of money in the economy, and the money supply declines. Similarly, if the government is not able to spend and its reserves in the central bank increase, the money supply declines in the market. The other demand-side factors of H are also affecting the money supply in the same way.

This H-Theory of money supply shows that money supply depends on H, and there are different factors affecting H, which directly or indirectly affect money supply. Though the central bank is said to have a dominant role in money supply, the central bank alone cannot control the money supply strictly. There are exogenous factors that the central bank cannot control in both the demand and supply sides of H. In the demand side of H, CP depends on the public choice, which the central bank cannot dictate or control. Similarly, RG depends on the final position and spending capacity of the government, which the central bank can suggest but cannot control. The only factors that the central bank can control on the demand side of H are RB, VCB, and RP.

On the supply side of H, NFA depends on remittance, tourism, foreign investment, and foreign aid, as well as foreign trade, which the central bank cannot control strictly. Similarly, in developing countries like Nepal, it depends on the government’s deficit financing policy. So, on the supply side of H, the central bank can control only CGE, CCB, and CPS. Therefore, the H-Theory of money supply shows that high power money positively affects money supply. So, the factors affecting H are also the factors affecting the money supply. The supply side factors of H positively affect the money supply, while the demand side factors of H inversely affect.

The money supply under this theory is determined jointly by the behaviour of the general public, government, BFIs, and the central bank because the central bank alone cannot control the whole money supply due to the nature of some factors that are exogenous to the central bank.

Money Multiplier

The theory of money multiplier shows that there is a positive relationship between money supply and money multiplier, where the money multiplier is a numerical value that shows by how many times the money supply increases due to an increase in a unit of High Power Money. Money Multiplier is expressed as the ratio of money supply and high-powered money, i.e.

Money Multiplier (m)= MS/H.

If we consider the narrow money supply(M1), we get marrow money multiplier(m1)as:

| m1 = M1/H |

| m1 = C + DD/C + R |

where,

C = Cash held by the general public

DD = Demand deposits in banks

R = Total Reserve in the banking system

Or,

Or,

This is the narrow money multiplier, which depends on C/DD and R/DD. If people start holding more cash (C/DD increases), the circulation of money declines, which reduces the value of the money multiplier and the money supply. Similarly, if the banks start holding more reserves (R/DD increases), it reduces the circulation of money, and so the value of the money multiplier and money supply declines. It means that C/DD and R/DD inversely affect the money supply. Likewise, if we consider Broad Money Supply (M2), we get the broad money multiplier (m2) as:

This is the broad money multiplier, which shows that the broad money multiplier depends on C/DD, R/DD, and TD/DD. C/DD and R/DD inversely affect the value of the money multiplier and money supply, whereas TD/DD and the money supply are positively related. It means if time deposits in the banking system increase, the banks are able to use the funds in the long term, which increases the circulation of money and the money supply. Therefore, the theory of the Money Multiplier shows that money supply inversely depends on C/DD and R/DD, whereas there is a positive relationship between money supply and TD/DD. However, these are the proximate determinants only. The ultimate determinants are the socio-cultural, behavioural, structural, and institutional factors. For example, C/DD depends on the behaviour of the general public, trust in BFIs, and access to BFIs, as well as the financial market and services.

Factors affecting money supply:

- High-powered money (H)

a) Demand side: CP< 0, RG< 0, RB< 0, VCB< 0, RP< 0

b) Supply side: NFA>0, NCG>0, CGE>0, CCB>0, CPS>0 - Money multiplier (m)

a) C/DD>0, b)R/DD>0, and c)TD/DD>0 - Others

a) Behavioral factors ( general public, government, and BFIs’ behavior)

b) Socio-cultural factors ( festivals, saving and consumption habits)

c) Seasonal factors ( seasonal economic activities like planting and harvesting)

d) Structural factors ( rural and urban structure, nature of economic activities, subsistence or modern)

e) Institutional Factors ( policies, laws, etc., eg, when CRR increases, then MS decreases )

f) Market development ( access and use of FinTech).

Determination of Money Supply in Nepal

Nepal Rastra Bank (NRB), being the central bank of Nepal, is responsible for managing the money supply so as to maintain the money market equilibrium, i.e., Money Supply equals Money Demand (MS = MD). If the money supply is more than the money demand, then there is excess liquidity in the market, which creates inflationary pressure, and NRB is not able to control inflation within the limit. Similarly, if the money supply is less than the money demand, then there is a liquidity crisis in the economy, which leads the economy to recession, or the growth target cannot be achieved. So, NRB determines the money supply so as to maintain the equality between money supply and money demand. Hence, NRB first estimates the money demand function using the time series data, which helps to estimate income and interest elasticity of money demand, which shows by how much money demand changes due to changes in income and interest rate. It is assumed that money demand is positive and proportional to the price level.

Once the money demand function is estimated, NRB considers growth and inflation targets based on the government budget. As the interest rate is assumed to be under the control of the central bank, the required growth rate of the money supply is estimated to achieve the targeted growth and control inflation within the limit. Assume that NRB tries to stabilize the interest rate at the existing level, or there is no change in the interest rate; then, NRB estimates the required growth rate of the money supply as below:

Required growth rate of money supply = Income Elasticity of money demand * Growth target + Inflation target.

Example,

Income Elasticity of money demand = 1.5

Growth rate = 6% and Inflation target = 5%,

Then,

Required growth rate of money supply = Income Elasticity of money demand * Growth target + Inflation target.

= 1.5*6+5

= 9+5

Required growth rate of money supply = 14%.

Once NRB estimates the required growth rate of the money supply to achieve the targeted growth rate and control inflation within a limit, then NRB estimates or forecasts the money supply growth based on certain assumptions regarding the sources and uses of the high-powered money and the money multiplier. For example, NRB forecasts remittance inflow based on certain assumptions in order to forecast NFA and money supply in the coming fiscal year. If such a predicted money supply growth and the estimated required growth of money supply are equal or almost equal, then NRB does not change the policy instruments. Otherwise, NRB uses expansionary or contractionary instruments in order to maintain the required growth rate of the money supply. So, NRB continuously observes the market and the money supply and makes necessary interventions if required through the policy instruments.

Factors to be considered in determining the money supply

While determining the money supply, the central bank has to consider various policies, laws, institutional, structural, and behavioural factors because the behaviour of the general public, governments, BFIs, and the policy of the central bank itself jointly determine the money supply. The following are the major factors to be considered:

i) Macroeconomic targets such as economic growth and inflation.

ii) Fiscal behaviour of the government, such as government expenditure, revenue mobilization, and domestic and external borrowing.

iii) Status and structure of the financial market, such as formal and informal.

iv) Development of financial market, financial technology, financial inclusion, and use of financial services.

v) Level of financial literacy and behaviour of the general public.

vi) Status of external trade, foreign investment, remittance, foreign aid, and tourism income and expenditure.

vii) Deficit financing policy of the government and spending capacity.

viii) Sectoral priority and policy of the economy, such as the agriculture sector priority, credit supply, deprived sector lending, etc.

ix) Credit carrying capacity of the private sector and the economy, such as the credit to GDP ratio, NPL, etc.

x) Domestic and external sector risk and vulnerability in the financial sector.

Conclusion:

Money Supply is defined as the total money in circulation within the economy during the given period. It is determined jointly by the behaviour of the general public, government, banks, and Financial Institutions (BFIs), and the policy of the central bank. Nepal Rastra Bank (NRB), being the central bank of Nepal, is responsible for managing the money supply so as to maintain the money market equilibrium, i.e., MS = MD. High-powered money and the money multiplier are the two primary determinants of the money supply, whereas behavioural factors, structural factors, institutional factors, socio-cultural factors, etc. are the secondary determinants of the money supply.